Capital One Pilots “Second Look”

Capital One recently launched a pilot for “Second Look,” a new service designed to provide automatic alerts for a number of unwelcome account activities. Recent e-mail communication and a web page dedicated to the pilot prove, yet again, Capital One has its fingers on the pulse – not only addressing customer needs, but also doing a serviceable job of promoting a difficult-to-explain solution while avoiding negative “big brother” associations.

What is Second Look?

A search on the Capital One website leads you to a single Q/A that is elusive in its description of the service yet provides big statement benefits to cardholders partaking in the Second Look pilot:

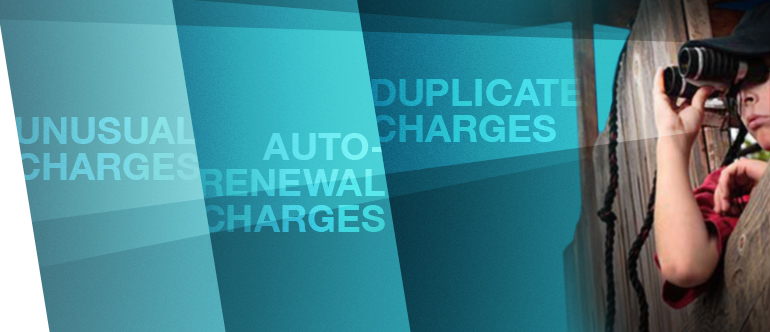

A first of its kind for major banks, Capital One is piloting a new free service that helps its customers identify unnoticed or potentially unwanted charges. Capital One Second LookSM goes beyond traditional fraud detection for Capital One card customers, flagging potentially duplicate charges, auto-renewing subscriptions and increases in recurring charges that are commonly overlooked. A service that is currently available to some card customers, Second Look will soon be available to all Capital One branded credit card customers with no need to sign up.

In addition to being free, benefits include its implied superiority and its status as a “first” among competitive banks. Capital One assumes that the pilot will have a successful outcome with roll-out to all cardholders in the future.

Capital One continues to weave marketing magic as only it can do – and we mean that as a compliment – by branding the new service and, even at this early pilot stage, linking it to a brand amplifying tag line: “It’s your money. We think you should keep it.”

The promotion of Second Look reminds us of challenges we’ve addressed in marketing similar services for other financial institutions. These services are intangible, technical and usually not new: it’s the application of the technology that is new, as with Second Look’s sniffing out higher-than-usual transactions or erroneous automatic recurring payments. Similar services – automatic travel alerts, mobile fraud alerts – require striking the perfect marketing balance between what sells and what scares. “Telling” too much could depress response when asking for participation in a feasibility study such as this.

Most likely, a copywriter struggled to describe this service without actually describing it – the net result are phrases like “Second Look spots… ” or “Capital One is keeping watch… ” attempting to define what goes on at the intersection of algorithms and data bases that keep tabs on your behavior and your transactions, like it or not.

What does Second Look do?

It appears that Capital One Second Look is not solidly defined in available communications. However, I was sure I could find a more exacting description of what the service does. According to the one web page I could locate and the consumer facing e-mail, the deliverables are kept high-level and Capital One is transparent in setting performance expectations for anyone who accepts the pilot invitation (quoted below):

Verify higher bill amounts

If we notice a typical recurring charge is higher than usual, we’ll let you know so you can confirm the payment amount is correct. Since this is a pilot, only some higher-than-normal bills may be identified initially.

Spot easy-to-miss charges

We’ll send you alerts about memberships and subscriptions that automatically renew annually. As this is a pilot program, only some easy-to-miss charges may be identified initially.

Avoid duplicate charges

We’ll raise a red flag by sending you an alert if it looks like you were accidentally charged twice for one transaction.

Capital One reached out to cardholders via e-mail (source: Competiscan*) in late August soliciting pilot participants and apparently targeting cardholders who are more likely to embrace the pilot since they are set up to receive real-time notices from the bank. Oddly, a recent blog post on Ask The Money Coach , calling Second Look a “cool new alert system,” has details on the service beyond what Capital One has pushed out cardholders.

Take-aways

Well done:

- Capital One has both named and developed a tagline giving the service an identity that is differentiated, ownable and compelling.

- Capital One leads with benefits statements and underscores that it is taking the burden from the cardholder while protecting their money.

- Capital One appears to be targeting the cardholder segment most likely to raise their hands to participate.

Could be better:

- At this early pilot stage, Capital One is promoting a third-party endorsement within its web page promotion for Second Look. Given that this is a pilot and still in the feasibility stage, this may be a misstep. On the very same marketing real estate, the bank is open about the possible limitations and the fact that this is a feasibility pilot; an endorsement feels out-of-place and lessens credibility. Instead, save The Money Coach testimonial for roll-out:

“Capital One just became the first U.S. bank to start giving customers email alerts about unexpected or questionable charges—like duplicate charges… ” – Lynette Khalfani-Cox, Personal Finance Expert, AskTheMoneyCoach.com

- To the likely audience – those who are already comfortable with tech-fraud solutions and mobile alerts – Capital One could take some steps to improve defining the service beyond its end benefit. Other explanations (like Visa’s description of its e-com fraud detection system) have made efforts to provide more background and build credibility for the back-end technology:

“… a data network that stores thousands of examples of valid purchase transactions and constantly updates cardholder data so future purchases can be evaluated against the most current profile. Each time an authorization request is processed, it’s evaluated against the individual’s transaction history.”

As more financial institutions provide increasingly complex solutions to detect, protect and communicate important information about account activity, brand positioning and messaging will continue to be challenging and critical to success. Our advice: keep it simple and positive, recognizing your cardholders are intelligent and welcoming of your proprietary solutions.

*Competiscan is a full-service, competitive intelligence market research firm that enables clients to study marketing and loyalty strategies by industry, company, product or recipient demographic. Media channels tracked include direct mail, email, online display, social media and print. Competiscan’s web-based search facility helps clients understand what consumers, business owners, financial advisors and insurance producers are viewing in the marketplace.