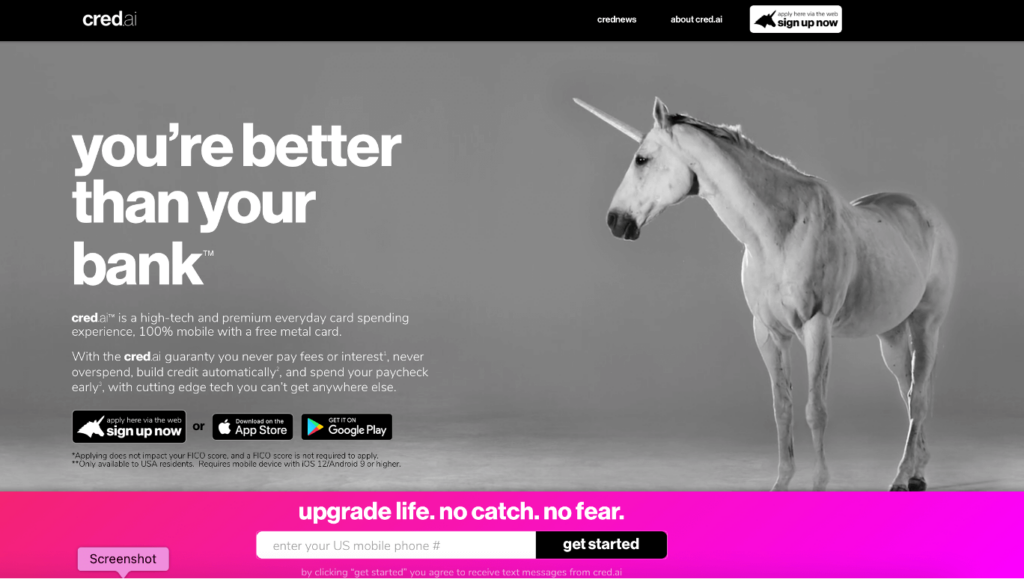

Cred.ai Unicorn Card: 5 Opportunities to Strengthen Card Acquisition Marketing

The fintech disrupter cred.ai and its Unicorn Card have been around since 2020. Still, according to this review in Forbes, there are only about 4K reviews for it on the Apple App Store versus 600K reviews for a competing product (Secured Chime Credit Builder), suggesting audience scale.

Assuming cred.ai’s acquisition success may not be as robust as its portfolio goals, we spotted opportunities to strengthen the fintech’s acquisition marketing – with broader application to fintech marketing in general. Although we don’t have insight into digital acquisition strategies and tactics, what is accessible – the cred.ai website – appears to have room for improvement in supporting conversion to the degree required.

1. Rethink the anti-bank positioning in the tagline: “You’re better than your bank.”

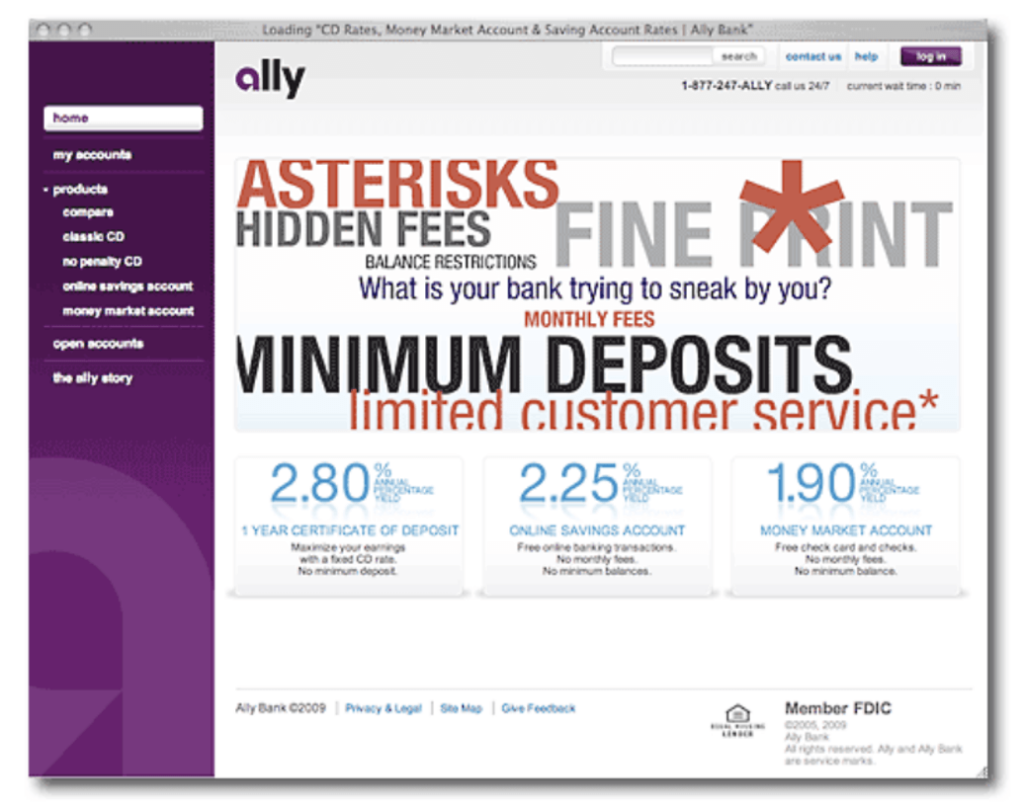

In 2011, Ally Bank started anti-bank campaigns with charm and relevancy while getting their point – unique at that time – and positioning across. It worked well and garnered industry attention.

Twelve years later, however, anti-bank positioning feels not only undifferentiated but also not relevant to all prospects nor for all bank products. It is now mainstream knowledge that fintechs, by design, provide an alternative to banks. And increasingly, fintechs work with banks to improve FI’s digital capabilities and offerings. With cred.ai’s intent to offer tech solutions beyond its current partnership with WSFS Bank, the tagline must evolve with cred.ai’s evolution.

Targeted cohorts – Gen Z, Millennials and Henry’s (high-earning not rich yet) – may not have deep relationships with traditional banks. Instead, they aspire to use a mix of payment products, knowing that credit cards are a necessity in life (if not right now, then in their future, despite the negative sentiments “credit” may evoke).

As they mature, this cohort is likely to spread their accounts across many financial institutions, including fintechs, credit unions and banks. Case in point, BAI research cited by The Financial Brand indicates loyalty to a single institution decreases with each U.S. generation: About 65% of Baby Boomers use one banking provider for their deposits compared with 44% for Generation X, 40% for Millennials and only 33% for Gen Z.

The solution: Often, fintechs can benefit from a second look at product positioning. Positivity and the cardholder payoff should drive the fintech brand and product positioning.

2. Use research to guide a better/consistent product definition.

Is this a credit card, debit card, secured card, new hybrid or none of the above? The audience with thin credit files and a need to build/rebuild credit scores may be clueless and unable to quickly connect with what cred.ai is offering, including the magic tech sauce that makes the card uniquely beneficial. In our experience, confusion and uncertainty readily translate to “not interested.”

Fintechs must challenge internal stakeholders and marketing agency partners to determine how best to define and describe their products. This may mean putting less emphasis on cool and more emphasis on clear and consistent.

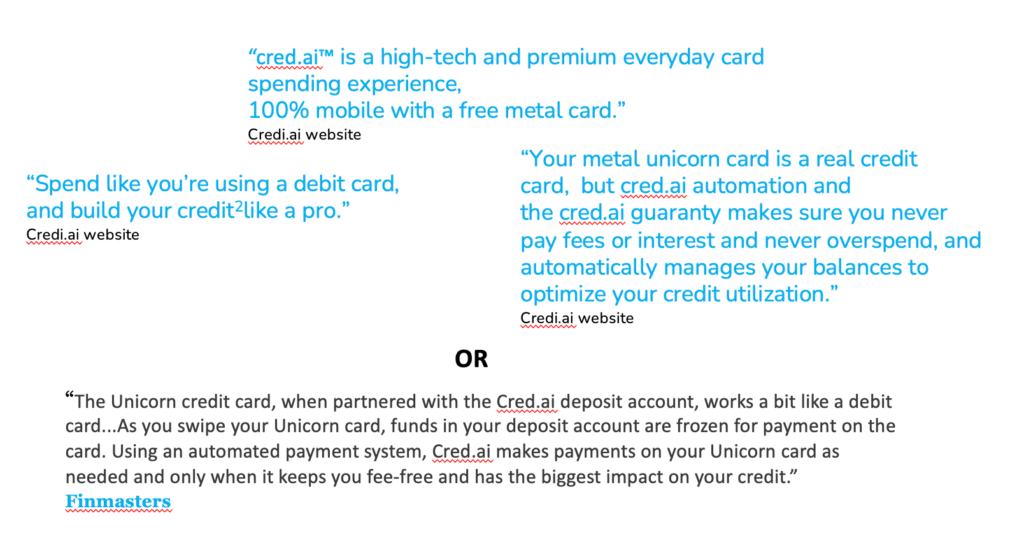

For example, Finmasters looked at cred.ai and did a good job defining the essence of the product, creating a possible jumping-off point for the exploration of new consumer-facing messaging:

When partnered with the Cred.ai deposit account, the Unicorn credit card works a bit like a debit card on a bank account. As you swipe your Unicorn card, funds in your deposit account are frozen for payment on the card. Then, using an automated payment system, Cred.ai makes payments on your Unicorn card as needed and only when it keeps you fee-free and has the biggest impact on your credit.

The tech-enhanced magic – highly associated with fintech success – must be well communicated. For example, cred.ai acts when and only when it is in the cardholder’s best interest, improving the management of payments from funds on deposit to impact a cardholder’s credit utilization positively.

3. Ban “premium” from the product vocabulary.

Dylan Brow, cred.ai’s president and co-founder, is quoted as saying the company’s mission is to “build a premium product for all people.” However, the use of “premium” in messaging to describe the card is at odds with the card’s reason for being. Premium implies “select,” which is diametrically opposed to the message of inclusion cred.ai must convey to reach its outsider audience.

A potential workaround to solve the disconnect between “it’s kind-of-a-secured-card” versus a “premium” card is simply to state the Unicorn card has some unexpected features and benefits that people assume are out of reach to credit-seekers. That allows prospects to feel good about the product without having them question the legitimacy of the premium claim.

As we have observed in working with brands, Fintech product messaging is not always as clear as it needs to be. Avoiding bank jargon is well understood, but fintechs often sacrifice the “how it works” as a way to skip long copy while offloading Gen Z/Millennial prospects to the small print. That’s not a best practice for obvious reasons.

4. Let the “about us” help, not alienate, your audience.

The cred.ai website is not deep in content, so every word really counts. From an outside perspective, we’d recommend pulling back on the mission statement, which is over the top.

We’re not in disagreement with the intent of cred.ai’s mission statement but honestly believe positivity would better serve the brand. Cred.ai knows what Intuit research has uncovered: “Quality of life is being held hostage by poor finances, especially for Gen Z Americans, the generation that values quality of life the most.” Clearly, cred.ai offers an alternative solution to being held hostage. Why not make the assertion and proof points both positive and optimistic?

5. Publish content that makes an impact, not “content because we can.”

It’s puzzling that cred.ai seems to be doggedly focused on broad news content – in fact, they assert cred.ai invests time and resources “because we can.” Cred.ai could really excel and differentiate itself by turning its talented content creators onto disrupting and elevating financial education. This is an area of focus and concern of Gen Z, and cred.ai has both the commitment to serve Gen Z and the talent to take financial education in new directions. (An aside: The website discloses that cred.news is the original content division of cred.ai. The disclosure is easily missed and not sufficient in rationalizing what is a general news feed on a credit card website.)

All fintechs have the opportunity to envision authentic disruption in financial education and consider how that movement might impact 67% of Gen Z consumers who feel like they will never have the things they want in life because of their financial situation. As noted in Intuit, “Yes, they have more access to financial information than any other generation, but this doesn’t always translate into decision-making.”

There are some other areas of opportunity, particularly on social platforms – IG, YouTube and TikTok – where content is engaging and surprisingly infrequent. A YouTube influencer shared sample content from the cred.ai mobile app, including friend-get-friend acquisition bonusing. Thinking back to a 2020 Forbes article about the upcoming card launch, the cred.ai Unicorn card was referred to as the “Tesla of banking” because creating the card required building a bank from scratch, according to their lead investor.

But Tesla was not an overnight success. Cred.ai – as well as many fintech start-ups – may require time and opportunity to focus on launching new offerings with other partners that target a wider range of consumers, as did Tesla, putting early struggles firmly in the rear-view mirror.